Superannuation returns have made for uncomfortable reading in recent months, but finally there is good news to share.

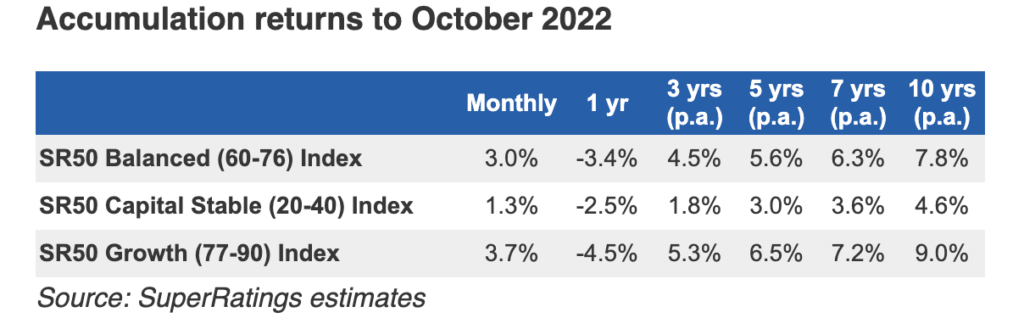

Superannuation research house SuperRatings estimates that the median balanced option for accumulation accounts generated a positive return of 3 per cent in October.

The positive return follows a -3.1 per cent result for the balanced option in September, a -0.5 per cent return for August and +0.5 per cent in July.

SuperRatings says the monthly ‘seesawing’ between positive and negative performance demonstrates how difficult it is to navigate the turbulent market environment and adds that “the bumpy ride is expected to continue”.

Read: Seniors card eligibility rules have changed

The median growth option increased by an estimated 3.7 per cent in October, while the median capital stable option, which has less exposure to share markets, delivered a smaller positive result, with a rise of 1.3 per cent.

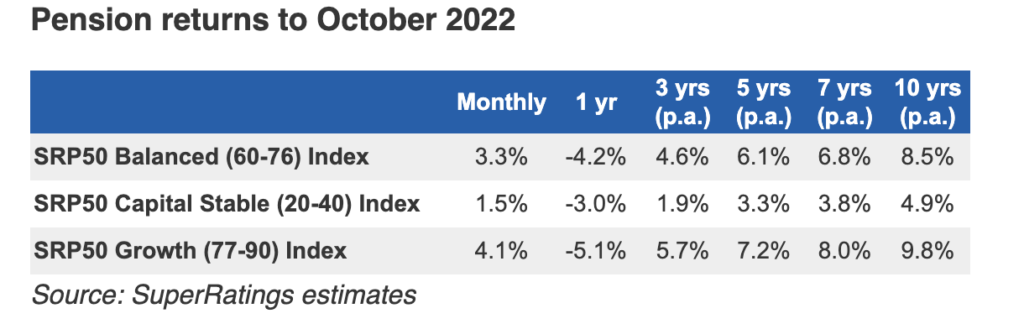

The good news extended to super pension accounts, with the median balanced pension option up an estimated 3.3 per cent. An increase of 4.1 per cent was estimated for the median growth option and 1.5 per cent for the median capital stable pension option.

SuperRatings executive director Kirby Rappell says it’s pleasing to see a 3 per cent return for members, but reinforces the importance of setting, and sticking to, a long-term strategy.

“Members who may have panicked and switched when returns were down last month may have missed out on this recovery,” he says.

“It is going to continue to be a bumpy road and focusing on these short-term indicators isn’t telling you the whole story. It’s best to consider your long-term objectives and the level of volatility you’re able to tolerate.”

Read: Work Bonus increase extended until end of 2023

He says that as we approach the end of the calendar year, it’s the perfect time to review your superannuation, talk to your fund or an adviser you trust and run a health check on your current settings to ensure your super is fit for the new year.”

Retirement confidence takes a battering

The welcome news is yet to change the mood of those in, or planning, retirement.

More than one in four (28 per cent) believe they won’t have enough super to stop work, according to a survey of 1057 Aussies. And three in five (62 per cent) are concerned about not having enough money in retirement.

Just 18 per cent believe they will have enough money to retire comfortably.

What’s more, almost one in two older Australians expect to outlive their retirement savings, according to a survey by Investment Trends of those aged 40-plus.

Add in new research by Money.com.au that finds almost one-third of people aged 35 to 60 expect to carry debt into retirement. Plus, Australian Bureau of Statistics data shows a sharp fall over the past two decades in the proportion of older Aussies who own their home outright.

What can you do?

For many, that all delivers a less-than-rosy outlook for retirement.

Finder superannuation expert Alison Banney says insufficient superannuation is a growing problem.

Most people aspire to retire in their mid-60s, but many don’t have enough for a comfortable retirement and cannot quit their job when they want to, she says.

“The cost of living crisis has made it especially hard to plan for,” she says.

The survey showed that men were much more assured about being able to retire, with 26 per cent confident they would have enough to live well in retirement compared to only 11 per cent of women.

Finder’s research revealed only 18 per cent make additional salary-sacrificed contributions to their super.

Read: Aussies expect superannuation shortfall

Ms Banney urges Aussies to pump up their retirement nest egg as soon, and as regularly, as possible.

“If you’re able to contribute a little bit extra to your super now, it will make a big difference by the time you retire,” she says.

“Making extra contributions isn’t the only thing you can do, though. The first step is to make sure you’re in a super fund that has low fees and a history of strong long-term performance.

“It’s also important to make sure you’ve only got one super fund in your name, so you’re not losing thousands of dollars to multiple sets of fees.

“If you have more than one, consolidate them as soon as possible.”

Are you tracking your super returns nervously or sitting back and looking to the long term? Have you had to change any retirement plans? Why not share your thoughts in the comments section below?

{kind=link}